In recent years, the pattern of China’s auto market has undergone a fundamental reversal. Chinese car brands have not only overtaken joint ventures (JVs) led by Volkswagen and Toyota in market share but also established core competitiveness in technology, cost and globalization. For global B2B new and used car buyers, understanding this shift is crucial for seizing market opportunities. This report analyzes the core reasons for the rise of China local brands with solid data and practical perspectives.

1. Market Pattern Reversal: From Catch-up to Leadership

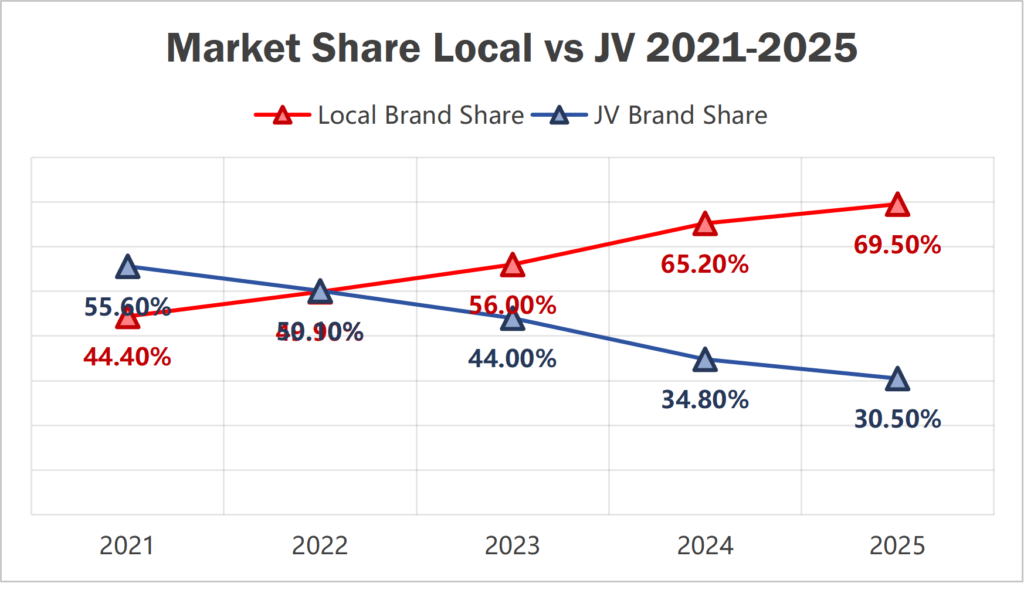

The market share gap between Chinese local brands and joint ventures has widened sharply since 2023. Data from the China Association of Automobile Manufacturers (CAAM) shows that local brands’ market share in China’s passenger car market rose from 44.4% in 2021 to 69.5% in 2025, while joint ventures fell from 55.6% to 30.5%. In the key 100,000-200,000 RMB price segment, BYD surpassed Volkswagen to become the leader in 2024, with its market share jumping from 13% in Q1 to 19% in Q4 <superscript:3>.

The following table clearly presents the changes in sales volume and market share of local and joint venture brands in the past five years:

| Year | Total Passenger Car Sales (10k units) | Local Brand Sales (10k units) | Local Brand Share | JV Brand Sales (10k units) | JV Brand Share |

|---|---|---|---|---|---|

| 2021 | 2148.2 | 953.8 | 44.4% | 1194.4 | 55.6% |

| 2022 | 2356.3 | 1176.6 | 49.9% | 1179.7 | 50.1% |

| 2023 | 2359.6 | 1321.4 | 56.0% | 1038.2 | 44.0% |

| 2024 | 2756.3 | 1797.0 | 65.2% | 959.3 | 34.8% |

| 2025 | 3010.3 | 2093.6 | 69.5% | 916.7 | 30.5% |

The following growth curve chart intuitively reflects the changing trend of market share between local brands and joint ventures from 2021 to 2025, which is more conducive to understanding the reversal of the market pattern:

As can be seen from the chart, local brands have maintained a steady upward trend in market share, surpassing joint ventures for the first time in 2023, and the leading advantage has expanded rapidly since then; joint ventures have shown a continuous downward trend, and the market share gap with local brands has widened year by year.

2. Core Reasons for Local Brands’ Rise: Four Key Drivers

2.1 New Energy & Intelligence: Changing the Game Rules

Local brands have achieved corner overtaking in the new energy track. In 2025, China’s new energy vehicle sales are expected to reach 15.65 million units, with local brands contributing over 80%. BYD‘s 5th-generation DM-i hybrid system achieves a thermal efficiency of 46.06%, with a fuel consumption of 2.6L per 100km and a comprehensive range of 2100km. In terms of intelligence, Huawei ADS 3.0 and Xpeng XNGP achieve 95% zero-takeover rate on roads, while most JV models still take CarPlay as a selling point and require additional payment to unlock L2-level assisted driving

BYD BLADE BATTERY

2.2 Cost & Industrial Chain: Solid Competitive Barrier

Local brands have a high degree of autonomy in the industrial chain, with the localization rate of core components exceeding 98%. The cost of three-electric systems (battery, motor, electronic control) is 20%-30% lower than that of JVs. Although JVs such as Volkswagen and Toyota have a vehicle localization rate of 75%-90%, they still rely on foreign parties for core technologies such as engine calibration and ECU, and the supply chain decision-making cycle is 3-5 times longer than that of local brands.

2.3 Product Localization: Precisely Meeting Market Demand

Local brands accurately grasp Chinese users’ needs for space and configuration. Compared with JV models of the same level, their wheelbase is generally 50-100mm longer, and they standardize L2 intelligent driving, 8155 chips and other configurations at the 100,000 RMB level. In contrast, JV models at the same price still provide cloth seats and mechanical instruments. In the after-sales service, local brands have a dense maintenance network, and the popularity rate of lifetime warranty for core components exceeds 80%.

2.4 Global Layout: Expanding Overseas Markets

In 2024, China’s auto exports exceeded 7 million units, of which new energy vehicle exports increased by more than 6 times. BYD’s overseas sales exceeded 1.0496 million units, a year-on-year surge of 145% . Local brands have established localized production systems in Brazil, Thailand and other regions, while JVs’ exports from China account for less than 5%, and their products are not optimized for emerging overseas markets.

3. Implications for Global B2B Buyers

For global B2B new and used car buyers, the rise of Chinese local brands means three major opportunities: first, cost-effective products with advanced technology; second, a complete industrial chain support and efficient after-sales service; third, localized solutions adapted to different markets. It is recommended that buyers focus on local brands’ new energy models and their global supply chain layout to gain more competitive advantages in the market.

In conclusion, the rise of Chinese local auto brands is not accidental but the result of long-term accumulation in technology, industrial chain and market operation. For global B2B buyers, adapting to this market change and cooperating with local brands will be an important strategy to win in the global auto market.

#AutoMarketTrends#ChinaAutoIndustry#B2BAuto#AutoExport#NewEnergyVehicles#ChinaCarExports#AutoIndustryInsights#AutoMarketAnalysis#EVIndustry